Hard Money Loan Closing: Step‑by‑Step Timeline for Fast Funding

Closing a hard money loan is the moment a deal moves from plan to payoff. This guide walks you through each step, explains the typical timeline, and lists the documents and costs you’ll need to close quickly and confidently. Many investors lose deals because they’re unprepared—knowing the process helps you avoid delays and seize opportunities when they appear. Below we cover the core steps, expected timing, required paperwork, closing costs, and practical tips to keep your transaction on track.

What Are the Key Steps in the Hard Money Loan Closing Process?

The closing process follows a clear sequence designed to protect both lender and borrower. Knowing these stages lets you prepare in advance and reduce surprises at the table.

- Initial Application: You submit the loan request with property details and basic financial information so the lender can start underwriting.

- Property Evaluation: The lender orders an appraisal or market evaluation to confirm the property’s value and loan risk.

- Loan Approval: With the valuation and documentation in hand, the lender decides whether to fund the loan and outlines final terms.

- Closing Preparation: Once approved, both sides assemble closing documents, confirm figures, and schedule the signing.

How to Prepare for Hard Money Loan Approval

Preparation shortens the path to funding. The items below are the most common ways to smooth underwriting and speed approval:

- Gather Documentation: Pull together bank statements, tax returns, and any income or asset verifications the lender requests.

- Understand Lender Requirements: Check the lender’s property standards, loan‑to‑value limits, and any credit or experience expectations before applying.

- Prepare a Business Plan: If this is an investment or rehab, outline your exit strategy, timeline, and cost estimates so the lender can see the plan for repayment.

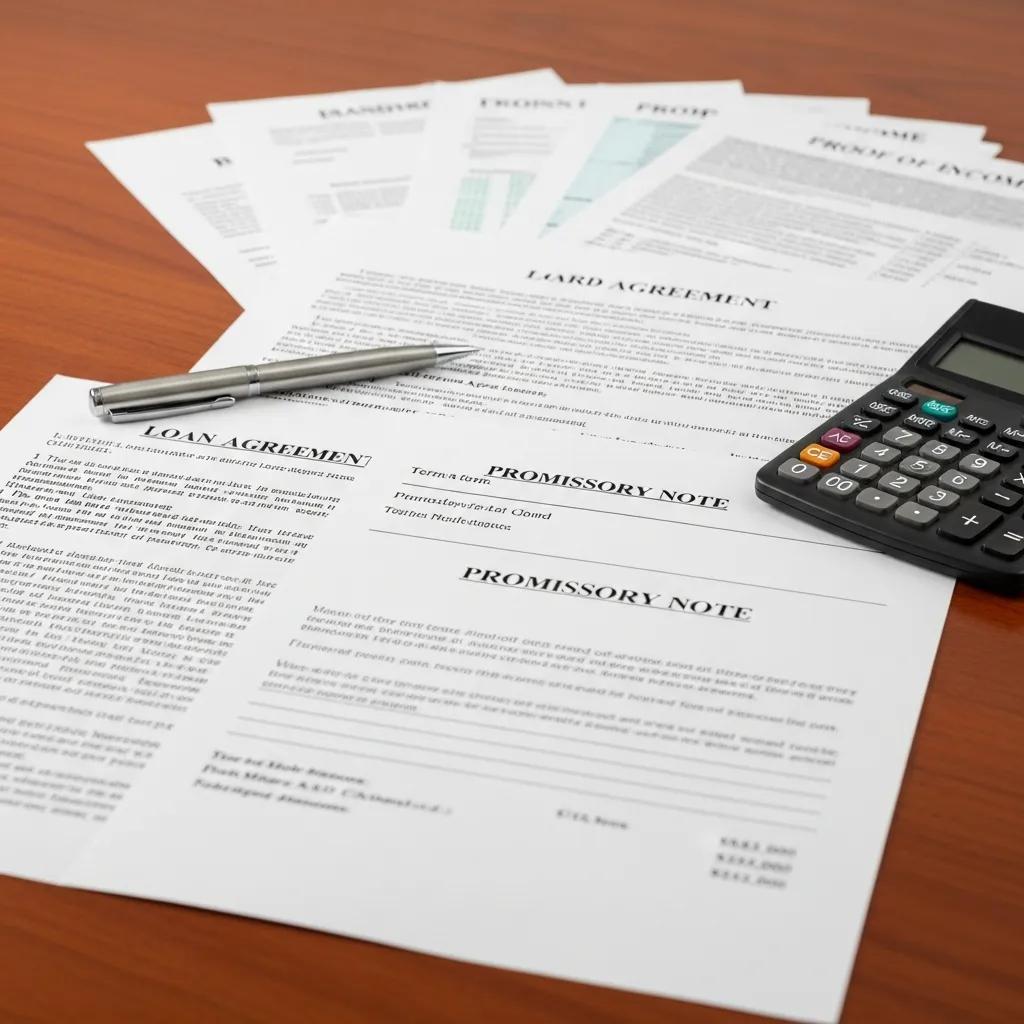

What Documents Are Required for Closing a Hard Money Loan?

Closing requires specific paperwork to finalize terms and protect both parties. The essentials are below.

- Loan Agreement: The contract that spells out the loan amount, interest, repayment schedule, and any fees.

- Promissory Note: Your written promise to repay under the agreed terms, including payment schedule and default consequences.

- Proof of Income: Recent pay stubs, bank statements, or other documents the lender uses to confirm your ability to perform under the loan.

How Long Does the Hard Money Loan Closing Timeline Typically Take?

Hard money closings are faster than traditional loans. Most transactions close in roughly one to two weeks, though several variables can speed or slow that timeframe.

Factors Influencing the Speed of Hard Money Loan Closings

- Lender Responsiveness: Fast communication and quick underwriting are the biggest drivers of a short timeline.

- Completeness of Documentation: Having all required documents ready prevents back‑and‑forth delays.

- Property Appraisal or Evaluation: Appraisal scheduling and reporting can add time, especially in busy markets.

How to Expedite Fast Hard Money Loan Funding?

- Choose the Right Lender: Work with lenders known for transparent terms and quick turnarounds.

- Pre-Approval: Get pre‑approved where possible so underwriting can begin faster when you find a property.

- Stay Organized: Keep documents accessible and respond promptly to requests to keep the process moving.

What Are the Common Hard Money Loan Closing Documents?

Familiarity with the main closing documents helps you review terms confidently and sign without hesitation.

Understanding the Loan Agreement and Promissory Note

These two documents form the legal backbone of the loan and deserve careful review.

- Loan Agreement: Details the loan amount, interest rate, fees, maturity, and any covenants or conditions between lender and borrower.

- Promissory Note: A binding promise to repay under the terms stated in the loan agreement, including interest and payment schedule.

What Additional Paperwork Is Needed at Closing?

Beyond the core loan documents, other records are commonly required at closing:

- Title Insurance: Protects the lender (and often the borrower) against title defects or ownership disputes.

- Closing Disclosure: A final accounting of loan terms and closing costs so both parties see the exact figures before signing.

What Costs Are Involved in the Hard Money Loan Closing?

Closing costs vary by deal, but these are the most typical charges you should plan for.

Typical Hard Money Loan Closing Costs Explained

Expect the following common expenses when budgeting for closing:

- Origination Fees: A lender fee for processing the loan, generally between 1% and 5% of the loan amount.

- Appraisal Costs: Fees to value the property, commonly in the $300–$700 range depending on scope and location.

- Title Insurance: Cost to insure the title against defects; often ranges from $1,000 to $2,000 based on property value and jurisdiction.

How to Budget for Fees and Expenses During Closing

Plan ahead with these practical steps:

- Estimate Total Costs: Add origination, appraisal, title, and any local or lender‑specific fees into your closing budget.

- Set Aside Funds: Keep reserves available so closing isn’t delayed by funding shortfalls.

How to Ensure a Smooth Hard Money Loan Closing Process?

Smooth closings come from preparation, clear communication, and timely execution. Use the tips below to minimize friction and avoid last‑minute issues.

Tips for Organizing Documents and Meeting Deadlines

Good organization saves time at closing:

- Create a Checklist: Itemize required documents, signatures, and deadlines so nothing is missed.

- Set Reminders: Calendar key dates—signing appointments, funding windows, and inspection deadlines—to keep everyone aligned.

Common Challenges and How to Avoid Delays

Watch for these typical snags and address them early:

- Communication with Lenders: Keep direct lines open—ask for a single point of contact and regular status updates.

- Timely Submission of Documents: Submit requested paperwork quickly; incomplete or late items are the most common cause of delays.

Knowing these typical costs ahead of time makes it easier to budget and close without surprises. When in doubt, ask your lender for a detailed estimate so you can confirm funds are available at signing.

Frequently Asked Questions

What is the difference between hard money loans and traditional loans?

Hard money loans are short‑term, asset‑backed loans usually provided by private lenders. Approval focuses more on the property’s value and the exit plan than on perfect credit. Traditional bank loans emphasize credit history, income verification, and take longer to close. Use hard money for speed and flexibility; use traditional financing for lower rates and longer terms.

Can I use a hard money loan for properties other than real estate?

Hard money is typically tied to real estate—residential, commercial, and investment properties are the norm. Some lenders may accept other collateral (equipment or vehicles), but that’s less common. Always confirm acceptable collateral with the specific lender before applying.

What happens if I default on a hard money loan?

If you default, the lender can foreclose on the property used as collateral. Hard money lenders often have faster foreclosure timelines than traditional lenders, so it’s important to have a clear repayment or exit strategy and to communicate early if issues arise.

Are hard money loans suitable for first-time investors?

They can be—especially when you need quick access to capital for a purchase or rehab. But first‑time investors should fully understand higher rates, shorter terms, and the need for a solid business plan. Work with experienced partners and run conservative numbers before committing.

How can I find reputable hard money lenders?

Start with referrals from real estate agents, brokers, or other investors. Check online reviews, ask for references, and verify licensing where applicable. Meet directly with lenders to discuss terms and ensure their process and timelines match your needs.

What are the risks associated with hard money loans?

Key risks include higher interest rates, short repayment windows, and the possibility of foreclosure if the exit plan fails. Market downturns can reduce property values, increasing your exposure. Mitigate risk with conservative financial planning, clear exit strategies, and working with transparent, experienced lenders.

Conclusion

Understanding the hard money closing process gives you control when speed matters. By knowing the steps, required documents, likely costs, and how to avoid delays, you can close faster and with confidence. If you need help assessing a deal or preparing documents, reach out to a knowledgeable lender or advisor—prepared investors close more deals.