Choosing a Hard Money Lender: The Practical Checklist Every Investor Needs

Picking the right hard money lender matters — it can speed a deal or sink it. This guide walks you, step‑by‑step, through what to look for so you can secure fast, flexible financing that fits your strategy. Hard money lenders evaluate property value first and borrower credit second, which makes them a different solution than conventional banks. Read on for the key selection criteria, the loan types investors use most, how the application process works, and answers to common borrower questions. When you finish, you’ll know how to choose a lender that suits your project and timeline.

What Is a Hard Money Lender and How Do They Differ from Traditional Lenders?

Hard money lenders make short‑term, asset‑backed loans secured by real estate. Their focus is the collateral — the property’s value and exit plan — not just your credit score. That shift lets them move faster and offer more flexible terms than traditional lenders, which is why investors turn to hard money when they need speed or are pursuing rehab and bridge strategies.

What Defines a Hard Money Loan and Its Key Features?

Hard money loans are asset‑based: the property’s value is the primary underwriting factor. Common characteristics include:

- Short-Term Duration: Typical terms run from about six months up to a few years.

- Higher Interest Rates: Because of the short term and higher risk, rates are generally higher than conventional mortgages.

- Quick Funding: Funding can often happen in days, enabling fast closings and timely project starts.

Those traits make hard money a practical choice when speed and collateral value are more important than long‑term financing.

How Does Asset-Based Lending Impact Loan Approval?

With asset‑based lending, approval hinges on the property’s equity and marketability. Lenders use appraisals, comps, and inspection findings to estimate value and upside, which speeds decisions and lets borrowers with imperfect credit still qualify. In short: strong collateral and a credible exit plan often outweigh a thin credit history.

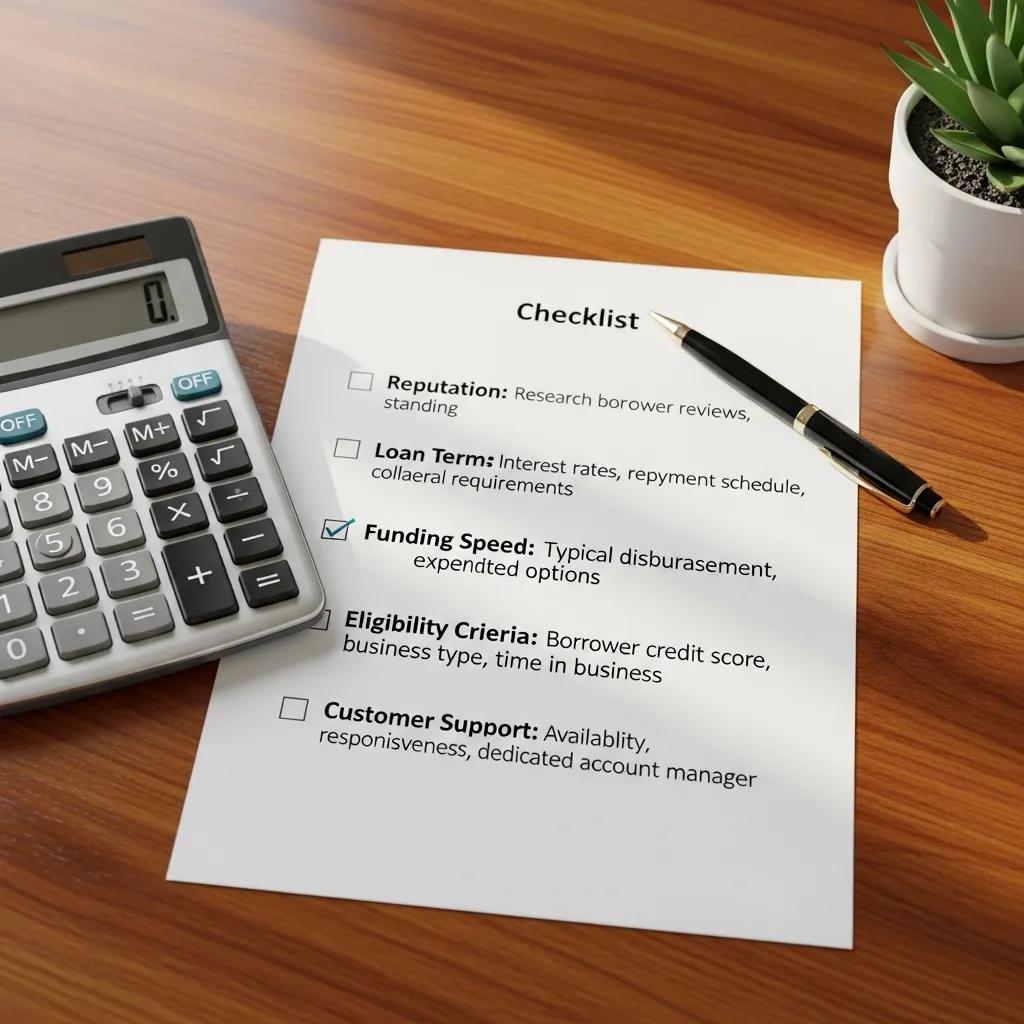

What Are the Essential Criteria for Selecting the Best Hard Money Lender?

Choosing a lender isn’t just about the rate. Focus on a few core factors to find the right partner for your investment:

- Reputation and Experience: Look for lenders with a proven track record and credible client feedback.

- Loan Terms and Fees: Compare rates, origination and servicing fees, and any other costs that affect your deal’s profit.

- Funding Speed: In competitive markets, the lender who closes fastest wins — confirm real turnaround times.

Evaluating these areas helps you pick a lender who supports your timeline and preserves your margins.

How to Evaluate Lender Reputation, Experience, and Local Market Expertise?

To vet a lender effectively, take these practical steps:

- Check Online Reviews: Read Google, industry forums, and borrower testimonials to gauge consistency and responsiveness.

- Ask for References: Request recent client references and specific project examples to verify outcomes.

- Evaluate Local Knowledge: Make sure the lender understands the markets where you invest — local comps and rehab costs matter.

Doing this due diligence reveals whether a lender can execute on deals in your target areas.

What Loan Terms, Interest Rates, and Fees Should You Compare?

When comparing offers, pay attention to the items that change project economics:

- Interest Rates: Seek competitive pricing that aligns with your exit plan. Hard money rates commonly range from 8% to 15%, depending on loan structure and borrower profile.

- Origination Fees: Upfront fees typically run from 1% to 5% of the loan amount — factor them into closing costs.

- Prepayment Penalties: Know whether early payoff triggers fees; that can affect refinance or resale decisions.

Comparing these elements side‑by‑side will show which offer truly fits your financial model.

Which Hard Money Loan Types Does Fidelity Funding Offer for Investors?

Fidelity Funding provides several hard money solutions designed for common investor needs. Knowing each option helps you pick the right product for your timeline and exit strategy.

What Are the Features of Purchase, Fix and Flip, and Bridge Loans?

- Purchase Loans: Provide immediate capital to close quickly and lock in deals.

- Fix and Flip Loans: Cover acquisition and rehab costs so you can renovate and flip for profit.

- Bridge Loans: Offer short‑term liquidity between transactions, giving you breathing room to arrange permanent financing.

Match the loan features to your timeline and exit plan to pick the most efficient financing route.

How Do DSCR Loans, Foreclosure Bailouts, and Commercial Loans Work?

- DSCR Loans: Underwritten on the property’s income potential — ideal for rental or income‑producing assets.

- Foreclosure Bailouts: Short‑term funds to acquire or salvage properties in distress and stabilize them for resale.

- Commercial Loans: Structured for business properties with terms and covenants tailored to commercial use.

Each product serves a specific strategy; choose the one that aligns with the asset type and your planned exit.

How Does the Hard Money Loan Application and Approval Process Work?

The hard money underwriting process is designed for speed and clarity so investors can execute quickly.

- Application Submission: You submit basic borrower info, deal details, and the property address.

- Property Evaluation: The lender orders appraisals, inspects the property, and runs market comps to size the loan.

- Approval and Funding: Once terms are agreed, funds can be disbursed within days — closing timelines depend on title and documentation.

That streamlined workflow is what makes hard money attractive for time‑sensitive deals.

What Documents Are Required and How Is Property Evaluated?

Typical documentation includes:

- Proof of Income: Statements or documentation showing your ability to support the loan or the project.

- Property Information: Photos, repair estimates, and details on current condition and market value.

- Credit History: While secondary to the asset, credit reports may still be requested for context.

Property evaluation relies on appraisals, inspections, and comps to confirm the collateral value and exit feasibility.

What Are Typical Approval Timelines and Funding Speeds?

Expect faster turnarounds than conventional lending:

- Approval Time: Often within 24–72 hours after a complete application.

- Funding Speed: Funds typically become available within three to seven days, depending on title and closing logistics.

These timelines let investors act decisively when opportunity strikes.

What Common Borrower Concerns Should You Address When Choosing a Lender?

Borrowers commonly worry about eligibility, costs, and downside risk. Addressing these concerns upfront helps prevent surprises during the deal.

- Credit Score Requirements: Many borrowers wonder whether credit will block approval.

- Property Eligibility: Knowing which properties qualify is essential.

- Foreclosure Risks: Borrowers want clarity on what happens if repayment issues arise.

Clear communication and realistic underwriting reduce uncertainty and build trust.

Is a Good Credit Score Necessary for Hard Money Loans?

Not usually. Hard money lenders prioritize the property and exit plan over FICO. A stronger credit profile can improve terms, but many lenders will approve borrowers with imperfect credit when the collateral and business plan are solid.

How to Assess Property Eligibility and Manage Foreclosure Risks?

Evaluate eligibility using these criteria:

- Property Type: Confirm the lender accepts the asset class — residential, commercial, or investment.

- Equity Position: Lenders look at current equity and loan‑to‑value to size the loan.

- Market Conditions: Local demand and comparable sales affect appraisal value and exit feasibility.

To reduce foreclosure risk, keep open lines of communication with your lender, maintain a realistic repayment plan, and have contingency options (refinance, sale, or partner buyout) ready.

Why Choose Fidelity Funding as Your Hard Money Lender Partner?

Fidelity Funding is built to move quickly and transparently for investors. We combine clear loan terms, timely funding, and personalized service so you can execute deals with confidence.

- Unique Benefits: Flexible programs and responsive underwriting that adapt to common investor needs.

- Client Success Stories: Real investors have closed time‑sensitive purchases and rehab projects using our solutions.

Those strengths make Fidelity Funding a practical partner for active investors who value speed and clarity.

What Unique Benefits and Flexible Programs Does Fidelity Funding Provide?

Key advantages include:

- Fast Approval Processes: Quick decisioning to help you close when opportunity arises.

- Tailored Loan Solutions: Programs structured around your strategy — whether purchase, rehab, or bridge financing.

- Expert Guidance: Our team provides honest, experienced feedback throughout the loan process.

These features help investors move deals forward without unnecessary delays or surprises.

How Have Client Success Stories Demonstrated Fidelity Funding’s Expertise?

Clients frequently cite timely funding and problem‑solving as reasons they chose Fidelity Funding. Investors have completed fix‑and‑flip projects, stabilized distressed assets, and bridged transactions to longer‑term financing — all backed by fast, reliable funding and pragmatic underwriting.

Frequently Asked Questions

What should I consider when comparing different hard money lenders?

Compare reputation, experience, loan structure, fees, and real funding speed. Read reviews, request references, and confirm actual closing times. Also review the lender’s flexibility around draw schedules, rehab budgets, and exit timelines to ensure the loan supports your plan.

Are there specific risks associated with hard money loans?

Yes. Higher interest rates and short terms can increase carrying costs if a project runs long. Borrowers may face pressure to refinance or sell quickly. If a borrower can’t perform, the lender can foreclose on the collateral. Clear exit planning and conservative underwriting reduce those risks.

How can I improve my chances of getting approved for a hard money loan?

Present a solid, realistic business plan: clear rehab budgets, accurate comps, and a defined exit strategy. Show property equity and documentation of income or assets. Good communication and complete paperwork speed underwriting and improve approval odds.

What types of properties are typically eligible for hard money loans?

Hard money can finance a wide range of assets — single‑family homes, multi‑family units, commercial properties, and investment rehab projects. Eligibility varies by lender; properties with clear upside and reasonable rehab plans are most likely to qualify.

What happens if I default on a hard money loan?

If you default, the lender can foreclose on the property used as collateral to recover the loan. That can mean losing the property and harm to your credit. The best defense is a realistic repayment plan, proactive communication with your lender, and contingency options should cash flow tighten.

Can I refinance a hard money loan into a traditional mortgage?

Yes. Many borrowers use hard money to acquire and improve a property, then refinance into conventional financing once the asset is stabilized and value is increased. Successful refinancing typically requires improved property value, satisfactory credit, and documentation that meets traditional lender standards.

Conclusion

Choosing the right hard money lender gives you speed, flexibility, and the ability to capitalize on deals. Know the criteria that matter — reputation, terms, and funding timelines — and match loan types to your exit strategy. Partnering with a lender like Fidelity Funding, which emphasizes transparency and quick execution, can help you move projects forward with confidence. Start comparing options now so you’re ready when the next opportunity appears.