Hard Money Loan Document Checklist — What You Need and How the Process Works

Hard money loans move fast — but the paperwork can slow you down. This guide breaks down, step by step, the exact documents lenders expect so you can submit a complete application and reduce delays. By the time you finish reading, you’ll know which forms matter most, how property documentation affects underwriting, what loan‑specific items to gather, and practical tips for organizing everything for a quick approval and funding. Many applications stall because files are missing or unclear; this checklist is designed to prevent that.

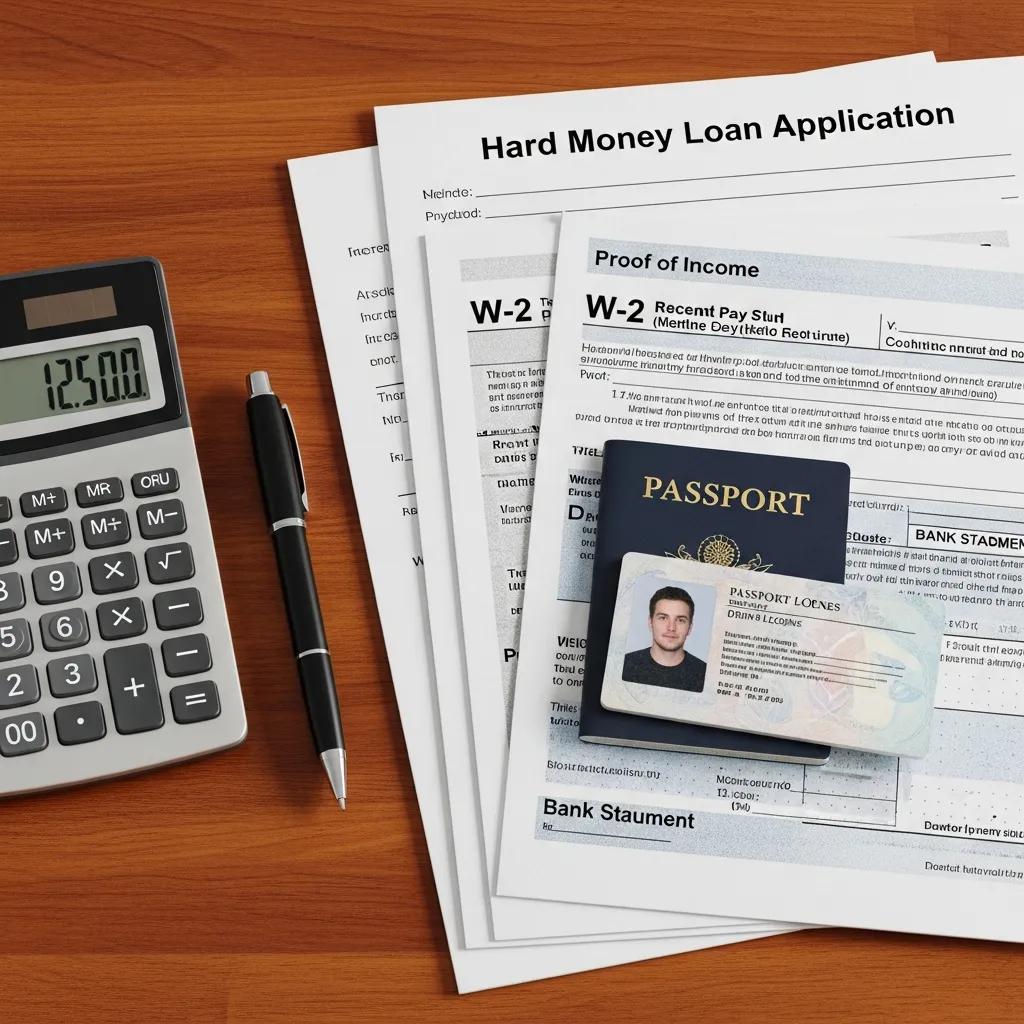

Which documents are essential for a hard money loan?

Hard money lenders focus on the collateral and the deal, but they still need core paperwork to evaluate risk and move quickly. Gather these items early to keep your application on track.

- Loan application: The primary form outlining the loan amount, purpose, and basic borrower information.

- Proof of identity: Government ID (driver’s license or passport) to confirm who you are.

- Proof of income: Recent pay stubs, tax returns, or bank statements. Some lenders rely more on property value than income, but these documents still help.

- Credit report: A summary of your credit history. Hard money lenders often weigh property value higher than credit score, but a credit report provides useful context.

Submitting complete, accurate documents up front shortens review time and improves your odds of a timely approval.

Which personal and business identification documents do lenders require?

Identification requirements vary slightly by lender, but typically include:

- Government‑issued ID: A current driver’s license or passport to verify identity.

- Social Security number: Needed for credit checks and tax reporting.

If you’re applying through an entity rather than personally, have these ready:

- Business license: Proof the entity is properly registered.

- Operating agreement: For LLCs, this shows ownership and management structure.

Any mismatch between IDs and application details can trigger delays — double‑check names, addresses, and EIN/SSN entries.

What financial statements and proof of funds should you prepare?

Lenders want to see evidence of financial capacity and funds for closing or reserves. Common documents include:

- Bank statements: Recent statements showing balances and cash flow.

- Tax returns: Personal and business returns for the prior two years when available.

- Proof of funds: Statements or investment account records proving you have down payment, reserves, or closing funds.

Having these items ready reduces back‑and‑forth and speeds underwriting.

How does property documentation affect your application?

Because hard money loans are secured by real estate, lenders scrutinize property value and condition. Clear, complete property records help lenders assess collateral risk and determine loan terms.

- Property appraisal: An independent valuation that confirms market value and informs loan‑to‑value calculations.

- Purchase contract: The signed agreement showing sale price and terms.

- Title report: Confirms ownership and flags liens or encumbrances that could affect lending.

Addressing title issues or appraisal gaps early prevents last‑minute surprises at closing.

What property details and photos should you submit?

Provide clear, thorough property information so underwriters can quickly evaluate condition and marketability:

- Property address: Full physical address for appraisal and title work.

- Property type: Specify residential, multi‑family, commercial, or industrial.

- Photos: Quality interior and exterior images that show current condition, damage, and key features.

High‑quality photos and accurate property data shorten the appraisal and inspection process.

Why are purchase contracts, appraisals, and title reports so important?

Each of these documents serves a distinct purpose in protecting both parties:

- Purchase contracts: Set the terms of the sale and anchor the loan amount to the transaction.

- Appraisals: Verify the collateral value that secures the loan.

- Title reports: Reveal legal claims that could affect lender recovery if a loan defaults.

Having them ready and accurate helps your file move swiftly to approval and funding.

What loan‑specific documents do different hard money loans require?

Loan purpose changes documentation needs. Below are common add‑ons depending on your loan type.

- Fix‑and‑flip loans: Renovation plans, contractor bids, and a realistic completion timeline.

- Construction loans: Blueprints, permits, and a construction draw schedule.

- Commercial loans: Detailed business financials and cash‑flow projections for the property.

Match your paperwork to the loan purpose so lenders can underwrite the project accurately.

Which documents are required for fix‑and‑flip and construction loans?

Typical requirements for these project loans include:

- Renovation plans: Scope of work and line‑item cost estimates.

- Contractor estimates: Bids from licensed contractors backing up your budget.

- Timeline: A clear schedule for milestone completion and expected sale or stabilization.

Construction loans will also ask for:

- Building permits: Proof you can legally begin work.

- Blueprints: Architectural plans that describe the intended build.

Accurate, contractor‑backed budgets and permits reduce lender risk and speed approvals.

What documentation is needed for commercial and DSCR loans?

For income‑producing or commercial deals, lenders require more detailed financials:

- Business financial statements: Profit & loss, balance sheet, and cash‑flow statements for the business for the last two years.

- Personal financial statements: Owner personal statements to support creditworthiness when required.

For DSCR (Debt Service Coverage Ratio) loans, include:

- DSCR calculation: Documentation showing property income versus debt obligations.

- Rental agreements: Existing leases or rental income statements to substantiate revenue projections.

Clear, verifiable income data helps lenders price risk and set loan structure appropriately.

How does knowing the application process help you prepare documents?

Understanding each step from submission to funding lets you anticipate requirements and avoid common delays. Below is the typical flow so you can organize accordingly.

- Application submission: Send your application and supporting documents to start underwriting.

- Review process: Lenders examine the file, order appraisals, and confirm title status.

- Funding: After approval and closing documents are signed, funds are disbursed per the loan terms.

Prepare paperwork ahead of time and respond promptly during review to keep the timeline tight.

What steps are involved from application to funding?

The common milestones are:

- Application submission: Provide the completed application and all initial documentation.

- Document review: Lender verifies documents and requests any missing items.

- Property appraisal: An appraisal or valuation confirms collateral value.

- Loan approval: Underwriting signs off on terms based on the file and appraisal.

- Funding: Closing occurs and funds are released so you can move forward with the project.

Being organized and communicative at each step shortens turnaround and reduces friction.

How does your exit strategy affect required documentation?

Lenders want confidence you can repay the loan. A clear exit strategy directly influences documentation and approval strength.

- Repayment plan: Show whether you’ll sell the property, refinance to permanent financing, or use rental income to pay the loan.

- Financial projections: Provide realistic projections that support your exit approach and demonstrate repayment ability.

A credible, well‑documented exit strategy can improve terms and lender confidence.

What legal and closing documents finalize your hard money loan?

Closing requires certain legal documents that protect both borrower and lender and record the loan against the property.

- Title documents: Confirm ownership and that the collateral is clear for lending.

- Escrow instructions: Direct the closing process and outline each party’s responsibilities.

- Mortgage documents: The note and security instruments that set loan terms and borrower obligations.

Having these items in order keeps the closing smooth and prevents last‑minute hold ups.

Which title, escrow, and mortgage documents are needed?

Standard closing paperwork includes:

- Title report: A detailed search that identifies liens or title issues.

- Escrow instructions: Written directions used by the escrow or settlement agent during closing.

- Mortgage agreement: The legal agreement listing interest rate, payment terms, and remedies for default.

Review these documents carefully and resolve any title or escrow items before closing.

What roles do promissory notes and personal guarantees play?

These legal instruments define the borrower’s repayment obligations and provide lender protections:

- Promissory note: The borrower’s written promise to repay the loan under the stated terms, including amount, interest, and schedule.

- Personal guarantee: When required, this makes an individual personally liable for the loan, adding a layer of security for the lender.

Understand these commitments before signing — they have long‑term implications if the loan does not perform as planned.

How can you ensure a smooth application with proper document organization?

Organization is one of the simplest ways to speed approval. Use a consistent system and back up your files to avoid delays.

- Create a checklist: Itemize every required document so nothing is missed.

- Use folders: Group files by category — IDs, financials, property, loan‑specific — for easy retrieval.

- Keep digital copies: Scan everything and keep a secure digital backup for quick resubmission.

A tidy, complete packet shows professionalism and makes the lender’s job easier.

What pro tips help you organize and submit loan documents efficiently?

Simple habits make a big difference:

- Label files clearly: Use descriptive file names and consistent labeling so items are easy to find.

- Maintain a timeline: Set internal deadlines for collecting documents and stick to them.

- Communicate with lenders: Stay responsive and clarify questions quickly to avoid hold ups.

These practices save time and reduce the chance of surprises during underwriting.

How does timely communication affect approval speed?

Fast, clear communication accelerates the review process:

- Prompt responses: Quick answers to lender requests keep momentum moving.

- Clarify questions: If anything is unclear, ask rather than guessing — it prevents rework.

- Provide regular updates: Let your lender know about changes to timeline, contractors, or finances so they can adjust without delay.

Open communication builds trust and often shortens the path to funding.

The table below summarizes the core documents lenders typically request and why each matters.

The following table highlights documentation tied to specific loan types so you can tailor your package.

Frequently Asked Questions

What is the typical timeline for a hard money loan application process?

Timelines vary, but a complete hard money application often closes within one to three weeks. Key factors are how complete your documentation is, whether an appraisal or title work is straightforward, and how quickly you respond to requests. Be proactive with paperwork and communication to keep things moving.

Can I apply for a hard money loan if I have a low credit score?

Yes. Hard money lenders emphasize the property and the deal more than personal credit scores. That said, expect to provide strong property documentation and proof of funds. Some lenders may still consider credit history when setting terms, so be transparent about your situation.

What are the common reasons for hard money loan application denials?

Denials most often result from incomplete documentation, insufficient collateral value, or a weak or unclear exit strategy. Discrepancies in financial records or unresolved title issues can also derail approval. Submitting a complete, well‑supported file reduces these risks.

How can I improve my chances of getting approved for a hard money loan?

Provide complete, accurate documents; present a clear exit strategy; and demonstrate the property’s value and potential. Clean title work, realistic budgets, and professional contractor estimates all increase lender confidence. Maintain fast, open communication throughout underwriting.

Are there any fees associated with hard money loans?

Yes. Expect origination fees, appraisal fees, and closing costs among others. Origination fees commonly fall between 1% and 3% of the loan amount, while appraisal costs depend on property size and location. Always review the loan estimate so you understand total borrowing costs.

What happens if I default on a hard money loan?

Hard money loans are secured by the property, so default can lead to foreclosure and the lender selling the collateral to recover funds. Because of that risk, lenders require clear exit plans and, in some cases, personal guarantees. If you foresee trouble, contact your lender early to explore options.

Can I refinance a hard money loan later?

Yes. Many borrowers refinance into conventional financing or another product once the property is stabilized or the borrower’s credit and equity position improve. Evaluate refinancing costs and timing to ensure it aligns with your financial goals.

Conclusion

Getting a hard money loan approved comes down to preparation: accurate IDs, clear financials, solid property documentation, and a realistic exit strategy. Organize your files, keep lines of communication open, and submit a complete packet to speed underwriting and funding. Start assembling your checklist now so you’re ready when the right deal comes along.