Hard Money Loan Application — Your Step‑by‑Step Path to Fast Real Estate Funding

When traditional lenders slow you down, hard money loans give you a faster route to capital by prioritizing the property’s equity over credit history. This guide breaks down the application from start to finish — what a hard money loan is, who it’s best for, the documents lenders want, and how to manage the loan after closing. Read through to gain a clear, practical plan for securing quick financing for your real estate investments.

What is a hard money loan — and when to use one

Hard money loans are short‑term, asset‑backed loans commonly used by investors who need speed and flexibility. Instead of relying mainly on your credit score, these loans are underwritten based on the property’s value, which lets you move faster on purchases and renovations when time matters.

The main advantages of hard money loans include:

- Fast approval: Lenders can approve deals in as little as 3–7 days, so you can act quickly when opportunity arises.

- Flexible eligibility: Credit requirements are often looser than with traditional lenders, widening access for many borrowers.

- Property‑first underwriting: The loan decision centers on the asset’s equity and marketability rather than solely on personal credit.

How hard money differs from traditional lending

Hard money and conventional loans diverge in a few important ways:

- Turnaround time: Conventional mortgages can take weeks or months; hard money is built for speed and can close in days.

- Qualification focus: Traditional lenders emphasize credit and income; hard money lenders emphasize the property’s value and exit plan.

- Cost of capital: Expect higher interest rates on hard money — commonly in the 8%–15% range — reflecting the lender’s increased risk and short term.

For investors who need quick, asset‑based financing, those tradeoffs often make sense.

Why investors choose hard money loans

Investors use hard money in a few common scenarios:

- Fix and flip projects: Fast funding lets you buy, renovate, and sell within tight timelines.

- Bridge financing: Use hard money as a short‑term solution while securing permanent financing.

- Foreclosure rescues: Hard money can enable purchases of at‑risk properties where speed is critical.

Each use case highlights the practical value of quick, property‑focused financing.

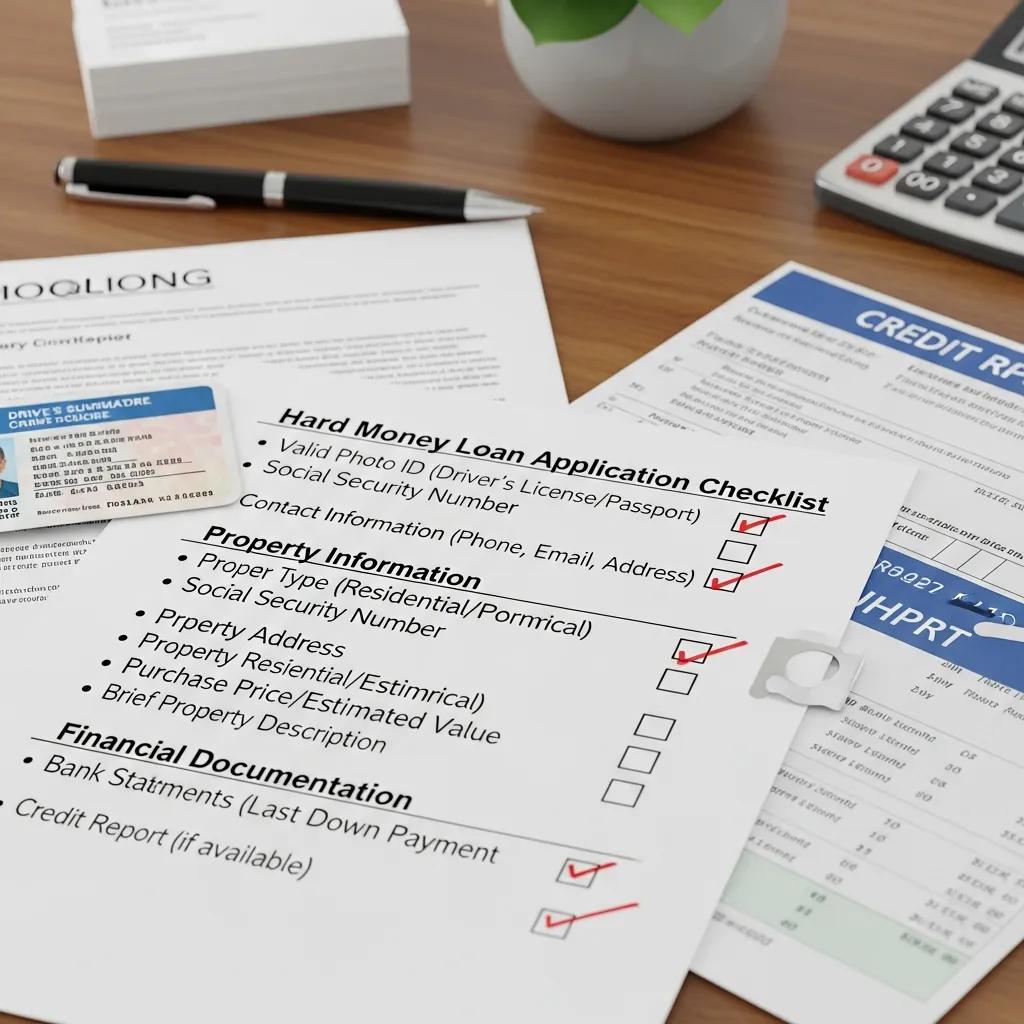

What lenders typically require for a hard money loan

Hard money applications look different from conventional loans. Knowing the usual requirements up front helps you prepare a cleaner, faster submission.

Which property and borrower factors matter most?

Lenders weigh several key factors when considering a file:

- Property type and equity: Both residential and commercial assets qualify, but lenders expect meaningful equity — commonly 20–30% or more.

- Borrower financial profile: While credit is less central, lenders still review income, assets, and experience to confirm repayment ability.

Those elements shape the lender’s assessment of loan risk and terms.

Documents you should have ready

Most hard money lenders will ask for these core items:

- Photo ID: A government‑issued ID to confirm identity.

- Property details: Address, condition notes, and any recent valuations.

- Financial records: Statements showing income, assets, and sources of funds.

Gathering these documents in advance will speed up pre‑approval and underwriting.

How the hard money application process flows

The process is designed for speed, but attention to detail still matters. Here’s how a typical application moves from inquiry to funding.

From first inquiry to pre‑approval: what to expect

Early steps usually include:

- Initial inquiry: Talk with a lender about your deal, timeline, and funding needs.

- Pre‑approval: Submit core documents so the lender can issue a preliminary approval and terms.

These stages often take only a few days when files are complete.

Property evaluation and underwriting explained

After pre‑approval, lenders will confirm the asset and borrower details through:

- Appraisal or valuation: An assessment to set loan value and loan‑to‑value limits.

- Underwriting review: A deeper look at finances, title, and the property’s condition to finalize terms.

Thorough evaluation ensures the lender can confidently fund the loan.

Reviewing offers, closing, and receiving funds

Once underwriting finishes, the lender issues a loan offer outlining rates, fees, and conditions.

How to evaluate rates, fees, and loan terms

When you get an offer, pay attention to:

- Interest rate: Compare the quoted rate to other short‑term options and factor it into your project budget.

- Fees and costs: Account for origination fees, points, closing costs, and any servicing fees that affect total cost.

Careful comparison of terms helps you choose the most cost‑effective solution for the deal.

Typical timeline for closing and funding

Closing steps generally include:

- Document signing: Final loan agreement and closing paperwork.

- Fund disbursement: After signing, funds are commonly wired within 1–3 business days.

That quick turnaround is one of hard money’s biggest advantages.

Specialized hard money loan programs you’ll see

Lenders offer tailored programs to match different investment strategies and property types.

Fix & flip, commercial, and bridge loan differences

Common product types include:

- Fix and flip loans: Short‑term financing built for purchase and renovation cycles.

- Commercial hard money: Structures and terms adapted for income‑producing or non‑residential properties.

- Bridge loans: Short‑term capital that fills timing gaps while you secure permanent financing.

Choosing the right program depends on your timeline, exit plan, and property type.

Foreclosure bailout and DSCR loan options

Other niche offerings to consider:

- Foreclosure bailout loans: Fast solutions that let investors or owners rescue at‑risk properties.

- DSCR loans: Underwritten to the property’s income (debt service coverage ratio), ideal for rental or commercial assets.

These options broaden the ways you can structure a deal around the asset’s cash flow or urgency.

Managing your hard money loan after closing

Once funded, proactive loan management protects your investment and preserves options for a smooth exit.

Common exit strategies for hard money loans

Investors typically use one of two exits:

- Sell the property: Complete renovations and sell to repay the loan.

- Refinance: Move to a traditional mortgage once the property’s value or cash flow stabilizes.

Pick the exit that best fits your hold period, market, and risk tolerance.

Avoiding prepayment penalties and planning repayment

To manage payoff effectively:

- Check for prepayment terms: Review the loan agreement for any early‑repayment penalties or time windows.

- Map your repayment plan: Build a timeline aligned with your renovation schedule, sale plan, or refinance target.

Planning ahead reduces surprises and preserves your returns.

Understanding each step of the hard money process puts you in control of your deals. With the right preparation and exit plan, hard money financing can be a practical tool for moving quickly on investment opportunities — whether you’re flipping a house or bridging to permanent financing.

Frequently Asked Questions

What risks should I expect with hard money loans?

Hard money delivers speed, but comes with tradeoffs: higher interest rates (typically 8%–15%), shorter terms, and the potential for foreclosure if repayment plans fail. Be mindful of fees and any prepayment restrictions, and make sure your exit strategy is realistic to manage those risks.

Can I use hard money for properties that need major repairs?

Yes. Lenders often underwrite to the after‑repair value (ARV) for rehab projects, so a solid renovation plan and budget are essential. Demonstrating how the upgrades increase value and providing realistic cost estimates will strengthen your application.

How do I pick the right hard money lender?

Evaluate lenders on reputation, responsiveness, fees, and experience with your property type. Ask for references, compare sample term sheets, and prioritize lenders who clearly explain their process and timelines. Specialization in your market or loan type can also be a major advantage.

What if I can’t repay my hard money loan?

If repayment becomes an issue, contact your lender immediately. Many will discuss options such as short extensions, modifications, or structured payoffs. Acting early and transparently gives you the best chance to avoid foreclosure and find an alternative exit.

Are hard money loans appropriate for first‑time investors?

They can be, but first‑time investors should proceed cautiously. Understand the costs, timeline, and risks, and have a clear plan for renovation, sale, or refinance. Partnering with experienced contractors, advisors, or a mentor can improve your odds of success.

How can I increase my chances of approval?

Put together a clean, detailed package: property photos, a realistic scope and budget for repairs, up‑to‑date valuations, and clear documentation of your financial position. A credible exit strategy — sale or refinance — is one of the strongest signals to a lender.

Conclusion

Hard money loans are a practical tool for investors who need speed and flexibility. By preparing the right documents, choosing the proper loan product, and lining up a reliable exit strategy, you can use asset‑based financing to capitalize on time‑sensitive opportunities. Start preparing your deal package now so you’re ready when the right property appears.