Points and Fees in Hard Money Loans — A Practical Guide for Real Estate Investors

When time matters, hard money loans can unlock deals — but the upfront costs matter just as much as the speed. This guide breaks down the points and fees you’ll encounter, shows how they affect your bottom line, and gives practical steps to calculate total loan costs. We cover origination and discount points, typical closing expenses, interest structures, and how to compare offers. Throughout, we explain how Fidelity Funding keeps fees transparent so you can move quickly without surprises.

What Are Points in Hard Money Loans and How Do They Affect Your Loan Costs?

Points are upfront charges tied to the loan amount and they change the effective cost of borrowing. Lenders typically charge origination points to cover loan setup and may offer discount points that prepay interest to lower your rate. Knowing the difference — and when each makes sense — helps you pick the financing that fits the timeline and return you’re targeting.

What Are Origination Points and How Are They Calculated?

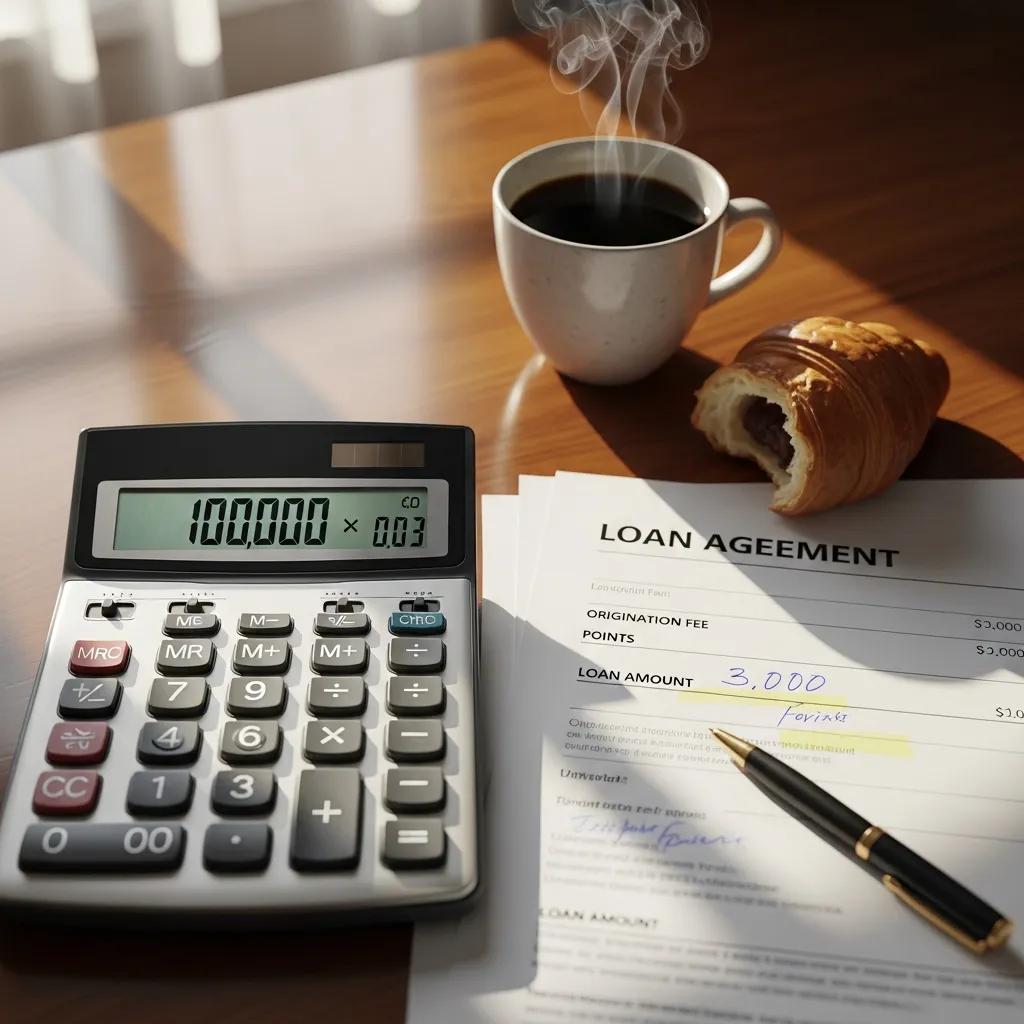

Origination points are fees the lender charges to process the loan. They commonly run from 1% to 3% of the loan amount. For example, a $100,000 hard money loan with a 2% origination fee costs $2,000 at closing. That fee covers underwriting, paperwork and the lender’s administrative work — and should be included when you model your deal.

What Are Discount Points and When Should Investors Consider Them?

Discount points are prepaid interest you buy to lower the loan’s rate. One point usually equals 1% of the loan and can reduce the rate roughly 0.25%–0.5% per point. So, on a $100,000 loan one discount point costs $1,000 and may save you thousands if you keep the loan long enough. Discount points make sense for investors who plan to hold or refinance rather than flip quickly.

What Are the Typical Closing Costs and Fees in Hard Money Loans?

Closing costs bundle a range of third-party and lender fees due at closing. They vary by lender, property and market, so build them into every deal analysis to avoid surprises.

Which Fees Are Included in Hard Money Loan Closing Costs?

Common closing costs you’ll see on a hard money loan include:

- Appraisal Fees: Payment for a property valuation used to set the loan amount.

- Title Insurance: Protection against title claims that could affect the lender’s lien.

- Escrow Fees: Charges for the neutral party that handles funds and documents at closing.

How Do Underwriting, Appraisal, Title, and Escrow Fees Impact Your Loan?

Underwriting fees cover the lender’s review of the borrower and the asset and are often a few hundred dollars. Appraisal, title and escrow fees add to the total closing bill. Combined, these costs commonly range from 2% to 5% of the loan amount — so on a $100,000 loan expect roughly $2,000 to $5,000 in closing expenses. Account for them up front when you evaluate ROI.

How Are Hard Money Loan Interest Rates and Fees Structured?

Hard money interest rates are higher than typical bank loans because private lenders assume greater risk and prioritize speed. Rates and fees depend on the property, the borrower’s experience and equity, and the loan-to-value ratio. Understanding those drivers helps you negotiate and compare offers effectively.

What Is the Average Interest Rate Range for Hard Money Loans in 2025?

As of 2024, hard money rates typically fall between 8% and 15%. Market conditions and deal specifics will shift that range, so get quotes from several lenders before you commit.

How Do Loan-to-Value Ratios and Borrower Profiles Influence Interest Rates?

Loan-to-value (LTV) and borrower profile are central to pricing. Lower LTVs reduce lender risk and usually lower rates; higher LTVs raise them. Likewise, experienced borrowers with solid track records can often secure better terms than first-time flippers or borrowers with sparse histories.

How Can You Calculate Your Total Hard Money Loan Costs Effectively?

To judge a loan fairly, combine points, closing costs and projected interest into a single cost model. That gives you a clear view of how the financing affects your project’s profit.

What Steps Are Involved in Calculating Points, Fees, and Interest?

Follow these steps to estimate total loan costs:

- Determine the Loan Amount: Confirm the principal you’ll borrow.

- Calculate Points: Multiply the loan amount by origination and any discount point percentages.

- Add Closing Costs: Include appraisal, title, escrow and underwriting fees.

- Estimate Interest Payments: Project total interest from the loan amount, rate and term.

How to Use a Hard Money Loan Calculator to Estimate Your Expenses?

Loan calculators speed this work. Enter loan amount, interest rate, points and term to get monthly payments and total cost estimates. Use several scenarios — different rates, points and hold periods — so you understand which financing path yields the best net return.

How Does Fidelity Funding Ensure Transparency and Avoid Hidden Fees in Hard Money Loans?

At Fidelity Funding we prioritize clear terms and up-front disclosures so you can evaluate deals quickly and confidently. That means straightforward fee schedules, transparent quotes and answers to the questions that matter to investors.

What Are Fidelity Funding’s Policies on Prepayment Penalties and Extension Fees?

We do not charge prepayment penalties, so you can pay off loans early without penalty. Our extension fee policies are disclosed up front, giving you the flexibility to plan for any potential extra costs before they arise.

How Does Clear Disclosure of Points and Fees Benefit Borrowers?

Transparent fee disclosure builds trust and enables better decisions. When borrowers see the full cost picture, they can compare lenders on a like-for-like basis and choose the financing that best supports their strategy.

How Do Points and Fees in Hard Money Loans Compare to Traditional Loan Costs?

Hard money is pricier up front and in rate, but it delivers speed and flexibility banks typically cannot. Weigh those tradeoffs against your project timeline and exit plan to decide which route maximizes returns.

What Are the Key Differences Between Hard Money and Traditional Loan Fees?

The main differences include:

- Higher Interest Rates: Hard money generally carries higher rates to reflect greater lender risk.

- Points Structure: Hard money loans often include more upfront points than traditional mortgages.

- Faster Processing: Where conventional loans can take weeks, hard money approvals can close in five to seven days.

How Can Investors Maximize ROI by Understanding These Cost Differences?

Match the loan to the deal: a quick flip can justify higher costs if it shortens hold time and increases turnover. For longer holds, lower-rate traditional financing may produce better returns. Running scenarios with all fees included lets you choose the most profitable path.

Different types of fees associated with hard money loans can significantly impact the overall cost of borrowing.

When you include these fees in your model, you avoid unexpected costs and can compare offers on equal footing.

In short, smart use of hard money depends on understanding both speed and cost. Know the points, anticipate closing costs, and model interest to see how the financing affects returns. Fidelity Funding aims to make those numbers clear so you can move confidently on the deals that matter.

Frequently Asked Questions

What is the difference between hard money loans and traditional loans?

Hard money loans are usually funded by private investors or specialty lenders and focus on collateral and deal economics rather than credit score alone. They close faster — often within days — and carry higher rates and fees than bank loans. That makes them ideal for short-term needs like flips or time-sensitive acquisitions, while traditional loans typically work better for long-term holdings.

Are hard money loans suitable for all types of real estate investments?

Hard money fits best for short-term projects, distressed buys or when speed is essential. It’s helpful for investors who need quick capital or who may not qualify for conventional financing. For buy-and-hold strategies, lower-cost traditional financing is often more economical over the long run.

How can I improve my chances of getting approved for a hard money loan?

Present a clear investment plan, show the property’s upside and equity, and demonstrate your exit strategy. Lenders focus heavily on the asset and its after-repair value, so detailed rehab plans, realistic budgets and a credible sale or refinance plan improve approval odds.

What should I look for in a hard money lender?

Choose lenders with a strong reputation, clear fee disclosure and experience in your market and asset type. Transparent communication, consistent underwriting and reasonable turn times are all signs of a reliable partner. Ask for references and read reviews from other investors.

Can I negotiate the terms of a hard money loan?

Yes — hard money terms are often negotiable, especially with repeat borrowers or on higher-quality deals. Focus negotiations on points, fees and rate, and be prepared to show why your project lowers lender risk. Still, expect some firm limits based on the lender’s criteria.

What happens if I default on a hard money loan?

Defaulting typically leads the lender to start foreclosure on the property used as collateral. Because hard money loans are asset-backed, lenders can move more quickly to protect their investment. To avoid default, keep an exit plan, maintain communication with your lender and explore modification options early if problems arise.

Conclusion

Understanding points and fees is essential to using hard money profitably. Build every fee and rate into your projections, compare multiple offers, and pick the financing that matches your timeline and exit plan. Fidelity Funding is committed to clear terms and fast closings so you can act on opportunities with confidence. Reach out to our team to discuss a tailored quote for your next deal.