SBA Loans vs. Hard Money for Commercial Property: A Clear Guide for Investors Who Need Speed and Certainty

Commercial real estate financing can feel complex — but it doesn’t have to be. This guide lays out the practical differences between SBA loans and hard money so you can pick the right tool for each deal. SBA loans, backed in part by the federal government, deliver longer terms and lower rates for qualifying borrowers. Hard money loans trade higher cost for speed, relying largely on property value to get capital in hand fast. We’ll walk through how each works, when one outperforms the other, and how Fidelity Funding structures hard-money options to help investors act quickly and confidently.

What Are SBA Loans for Commercial Real Estate?

SBA loans are government‑backed programs that help small businesses buy or refinance commercial property. Because the Small Business Administration guarantees a portion of the loan, lenders can offer longer amortizations and more competitive rates than many conventional products — making SBA loans an attractive fit when you qualify and can wait for a full underwriting process.

What Defines an SBA Loan and Its Government Guarantee?

An SBA loan includes a government guarantee from the Small Business Administration that reduces lender risk on a portion of the loan. That guarantee is what allows lenders to approve borrowers who might not meet stricter conventional criteria. Typical borrower benefits include lower down payments and extended repayment windows, which ease monthly cash flow for owner‑operators.

How Do SBA 7(a) and 504 Loans Differ for Commercial Properties?

The two most common SBA programs for real estate are the 7(a) and 504 loans. The 7(a) is flexible — it can finance purchases, refinance debt, or support working capital — while the 504 is aimed at fixed assets like owner‑occupied buildings and often pairs a certified development company with a private lender. They differ in maximums, rate structures, and eligibility rules, so select the program that aligns with your property type and business needs.

How Do Hard Money Loans Work for Commercial Property Financing?

Hard money loans are short‑term, asset‑backed loans designed for investors who need capital quickly. Approval centers on the collateral — the property — rather than deep credit underwriting. That property focus and streamlined process make hard money well suited to time‑sensitive purchases, renovations, or situations where conventional financing isn’t practical.

What Are the Key Features of Hard Money Loans?

- Speed of Funding: Hard money can close in days rather than weeks, which matters when timing makes or breaks a deal.

- Flexibility in Terms: Lenders can tailor terms and repayment structures to fit the project timeline and exit strategy.

- Focus on Property Equity: Underwriting hinges on the asset’s value and potential, giving borrowers with imperfect credit a path to capital.

Which Commercial Property Uses Benefit Most from Hard Money Loans?

- Fix and Flip Projects: Fast purchase and rehab funding lets investors complete short‑cycle renovations and exit on schedule.

- Bridge Loans: Temporary financing covers an acquisition or hold period while you arrange longer‑term capital.

- Foreclosure Rescues: Quick closings let buyers move decisively on at‑risk properties in competitive auctions or short sales.

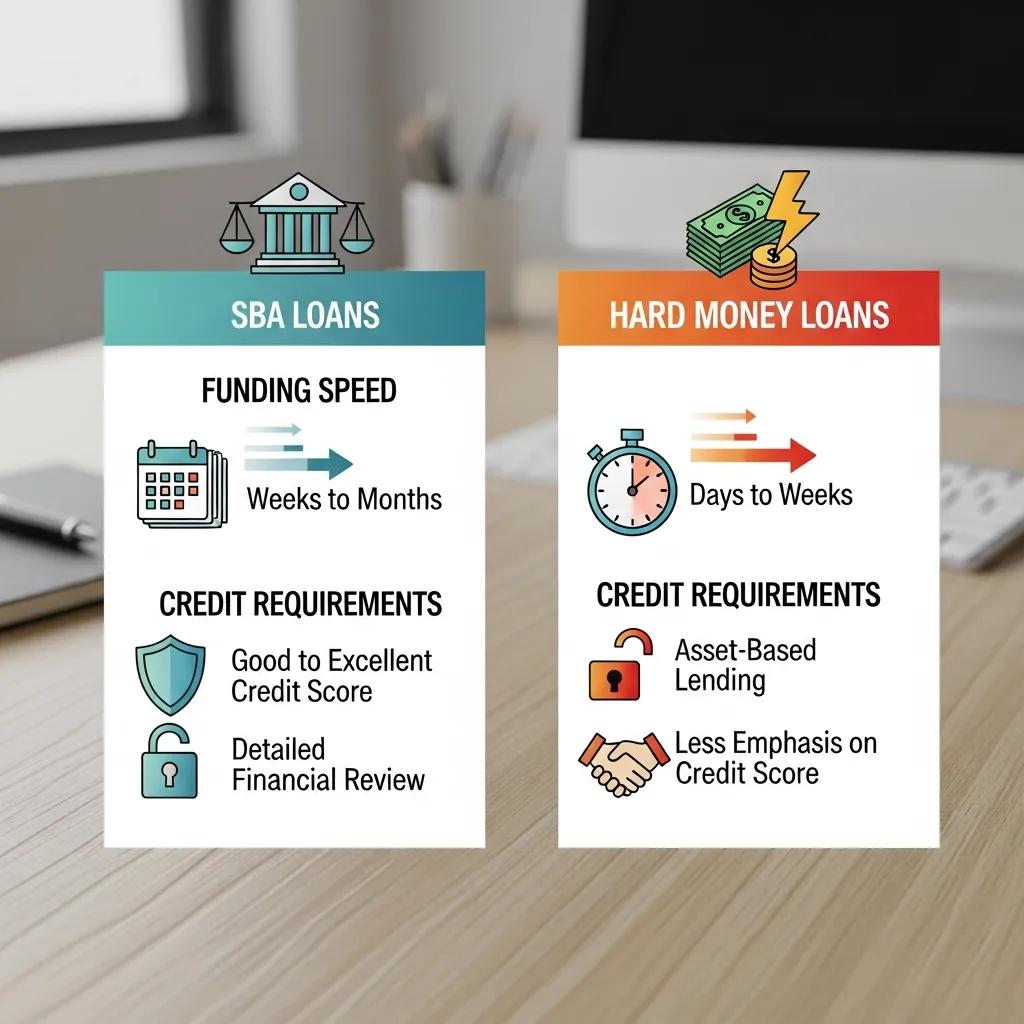

What Are the Main Differences Between SBA Loans and Hard Money Loans?

Both loan types serve commercial investors, but they solve different problems. SBA loans are cost‑effective for qualified borrowers who can tolerate a longer approval timeline. Hard money prioritizes speed and collateral value, making it useful when time, credit, or occupancy rules block conventional options.

How Do Funding Speed and Approval Timelines Compare?

Timing is a core distinction. SBA financing generally requires a multi‑week underwriting cycle — commonly 4 to 8 weeks or longer. Hard money lenders, by contrast, can underwrite and fund in as little as a few days, which is why they’re the tool of choice for urgent acquisitions.

What Are the Credit and Documentation Requirements for Each?

SBA loans typically demand extensive documentation and a solid business credit profile. Hard money shifts the emphasis to the property’s value and exit plan, allowing for lighter personal credit review and faster documentation — though at a higher cost and shorter term.

How Does Fidelity Funding Provide Fast, Flexible Hard Money Solutions?

Fidelity Funding focuses on pragmatic hard‑money lending for investors who need predictable timelines and transparent terms. We prioritize clear communication and rapid decisions so borrowers can move on opportunities without unnecessary delays.

Which Commercial Loan Programs Does Fidelity Funding Offer?

- Fix and Flip Loans: Short‑term capital for acquiring and renovating properties with an eye toward quick resale.

- Bridge Loans: Interim financing to cover acquisition or holding periods while you arrange permanent funding.

- Long‑term Hard Money Loans: Structured options for investors who plan to hold assets longer but prefer flexible underwriting.

What Are the Simple Approval Steps and No Prepayment Penalties?

We keep approval straightforward so you can focus on the deal, not paperwork. Typical steps include:

- Application Submission: Provide basic borrower and property information to start underwriting.

- Property Evaluation: We assess the asset and projected market value to set loan terms.

- Loan Approval: On approval, funds are disbursed quickly so you can close on schedule.

Fidelity Funding does not charge prepayment penalties, so you can refinance or pay off the loan early without surprise fees.

When Should Investors Choose Hard Money Over SBA Loans?

Choose hard money when speed, flexibility, or property‑centric underwriting is essential to the transaction. It’s the practical solution for short windows and complex borrower profiles.

How Do Time-Sensitive Deals and Bridge Loans Favor Hard Money?

When auctions, contingency deadlines, or rapid price movements demand immediate action, hard money delivers capital on a timeline that conventional programs cannot match. It’s also the default for short‑term bridge financing.

How Can Hard Money Help Overcome Credit and Owner-Occupancy Challenges?

Hard money is useful when credit scores, business history, or strict owner‑occupancy rules rule out SBA or bank financing. Because decisions center on the asset and exit plan, qualified investors can move forward even with imperfect underwriting profiles.

What Are the Key Considerations for Commercial Property Financing?

Before choosing a product, assess the project timeline, exit strategy, cash‑flow needs, and tolerance for rate and term trade‑offs. Those factors will point you to the most appropriate financing route.

How Do Loan-to-Value Ratios and Leverage Impact Financing?

Loan‑to‑value (LTV) determines how much capital you can access versus equity required. Higher LTV increases leverage and purchasing power but also raises risk if market values shift. Match LTV to your risk tolerance and exit plan.

What Benefits Do Investors Gain from Speed, Flexibility, and Terms?

Speed lets you seize fleeting opportunities. Flexible terms allow you to align payments with project milestones and exit timing. Both are critical in competitive markets where timing, not just price, determines success.

SBA and hard‑money loans each offer clear benefits and trade‑offs. The right choice depends on your timeline, credit profile, property type, and long‑term strategy.

This side‑by‑side shows how funding timelines and underwriting focus differ — use it to match the loan to your deal dynamics.

Weigh funding speed, credit needs, and your project timeline when choosing between SBA and hard‑money financing. Clear priorities make the right option obvious.

Frequently Asked Questions

What are the typical interest rates for SBA loans and hard money loans?

SBA loans generally carry lower rates — commonly in the 5%–8% range depending on program and borrower credit. Hard money rates are higher, often between 8% and 15%, reflecting the shorter terms and faster funding. The premium for hard money buys speed and looser credit requirements.

Can SBA loans be used for refinancing existing commercial properties?

Yes. SBA programs — notably the 504 — can be used to refinance existing debt and acquire fixed assets. Refinancing with an SBA product can lower monthly payments or extend terms, but eligibility and program specifics vary, so consult a lender for details.

What are the risks associated with hard money loans?

Hard money carries higher interest and shorter terms, which can strain cash flow if a rehab or exit takes longer than planned. There’s also the risk of market‑value fluctuations that affect refinance or resale options. Evaluate your exit plan and stress‑test timelines before committing.

How does the approval process differ between SBA loans and hard money loans?

SBA underwriting is more thorough and documentation‑heavy, often requiring weeks to complete. Hard money underwriting focuses on property value and the exit strategy, so approval can be much faster — frequently within days.

Are there any prepayment penalties associated with SBA loans?

Some SBA loans include prepayment provisions, particularly during early years, to protect lender interest income. Terms vary by loan and lender, so review the agreement carefully. Fidelity Funding’s hard‑money products do not carry prepayment penalties.

What types of properties are eligible for SBA loans?

SBA loans typically finance owner‑occupied commercial properties — offices, retail, warehouses, and light industrial facilities — where the business occupies at least 51% of the space. That owner‑occupancy rule distinguishes SBA financing from many investor‑focused products.

How can investors determine which financing option is best for their needs?

Start with your timeline and exit plan. If low rate and long term are priorities and you meet eligibility, SBA can be the smarter, cheaper choice. If speed, flexibility, or non‑standard borrower profiles are the constraint, hard money is often the right short‑term solution. Speak with a lender or advisor to align financing with your project goals.

Conclusion

Knowing the strengths and limits of SBA versus hard‑money lending helps you choose the right capital for each deal. SBA loans offer long‑term stability when you qualify; hard money delivers speed and asset‑driven underwriting when time or credit issues matter most. Match the loan to your timeline, risk tolerance, and exit strategy — and when speed is the priority, Fidelity Funding can provide clear, fast, and flexible hard‑money solutions to get your deal across the finish line.